The entry into force of the Corporate Sustainability Reporting Directive (CSRD) marks a decisive turning point in the European regulatory framework for non-financial reporting. The CSRD, which replaces the Non-Financial Reporting Directive (NFRD), aims to improve the transparency and consistency of environmental, social and governance (ESG) information published by companies. This new directive, effective from January 1, 2024, considerably expands the number of companies covered by non-financial reporting obligations.

Understanding CSRD

Definition and objectives of CSRD

The Corporate Sustainability Reporting Directive (CSRD) is a European directive that reinforces the non-financial reporting obligations of companies. It aims to improve the quality and transparency of environmental, social and governance (ESG) information provided by companies. By establishing clear, harmonized standards for reporting, the CSRD aims to make it easier for companies to compare their ESG performance, and to boost the confidence of investors and other stakeholders.

The main objectives of the CSRD include :

Increased transparency: Provide more detailed and comparable information on companies' ESG performance for investors, regulators and the general public.

Standardized reporting: Establish uniform Europe-wide reporting standards to ensure consistency and comparability of data.

Strengthening sustainability: Encourage companies to adopt sustainable practices and integrate ESG considerations into their business strategy.

Regulatory compliance: Ensure that companies comply with their ESG reporting obligations, thereby contributing to a more sustainable economy.

From NFRD to CSRD

The CSRD replaces the Non-Financial Reporting Directive (NFRD), in force since 2014. The NFRD had introduced the first extra-financial reporting obligations for major European companies. However, its limitations in terms of scope and clarity of information led to the need for an in-depth revision.

The main changes introduced by the CSRD compared with the NFRD are as follows:

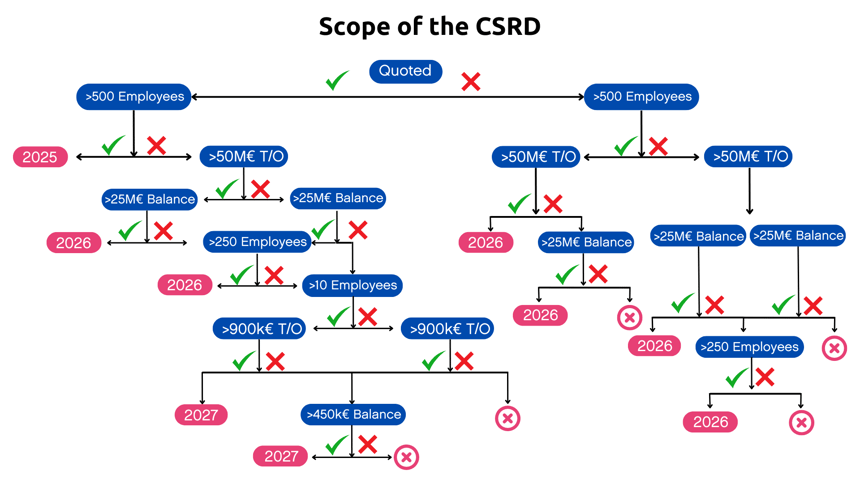

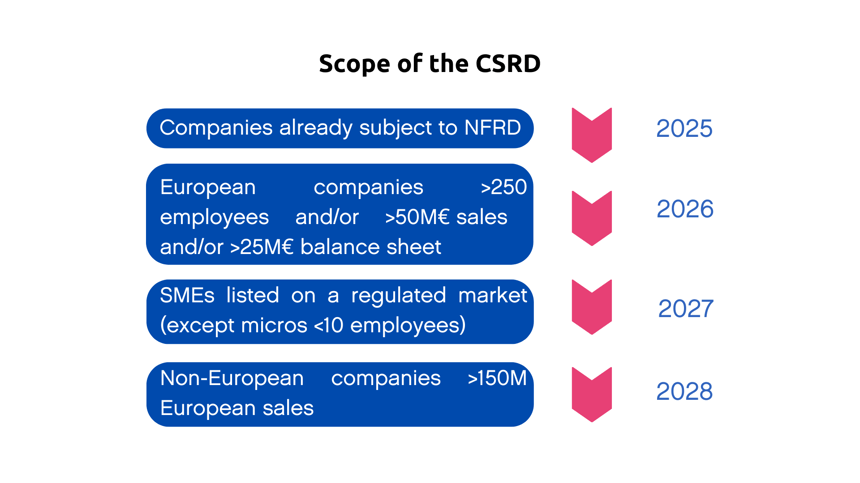

Extended scope: Whereas the NFRD applied mainly to large companies and public interest entities with more than 500 employees, the CSRD extends this obligation to a wider range of companies, including listed SMEs and subsidiaries of non-European companies operating in Europe.

Stricter reporting standards: The CSRD introduces more detailed and specific standards for ESG reporting, based on the European Sustainability Reporting Standards (ESRS). These standards cover a wide range of environmental, social and governance criteria.

Audit and assurance: The CSRD imposes stricter requirements for the audit and verification of ESG information, aimed at ensuring the accuracy and reliability of reported data.

Digital reporting: Companies are encouraged to use digital formats for their reporting, making it easier for stakeholders to access and analyze data.

Double materiality: The CSRD emphasizes the concept of double materiality, requiring companies to assess not only the impact of their activities on the environment and society, but also how ESG issues affect their financial performance.

Companies concerned by CSRD

Large companies

The CSRD applies mainly to large companies. Specific criteria for a company to be considered large and subject to CSRD obligations include:

- Employees: The company must have more than 250 employees.

- Sales: Sales in excess of 40 million euros.

- Balance sheet total: A balance sheet total exceeding 20 million euros.

These criteria are designed to ensure that companies with a significant impact on the economy and the environment are required to provide detailed information on their ESG performance. The directive aims to improve the transparency and accountability of large companies, which often have a considerable environmental and social footprint.

Listed SMEs

In addition to large companies, the CSRD also extends to listed small and medium-sized enterprises (SMEs). Although these companies generally have fewer resources than large corporations, their inclusion in the CSRD reflects the growing importance of ESG transparency in financial markets. Application criteria for listed SMEs include :

- Listed: SMEs must be listed on a regulated market in the European Union.

- Temporary exemptions: Listed SMEs have a temporary exemption and must comply with reporting obligations from 2026, giving them more time to prepare for the new requirements.

Subsidiaries and branches of non-European companies

The CSRD also applies to subsidiaries and branches of non-European companies operating in the European Union. The criteria for these entities are as follows:

- Sales in Europe: Subsidiaries or branches of non-European companies must generate sales in excess of 150 million euros in the European Union.

- Significant impact: These entities must have a significant impact on the environment and society in the regions where they operate, thus justifying the application of ESG reporting standards.

Reporting obligations and ESG standards

ESG indicators required

The CSRD imposes rigorous reporting obligations focused on ESG criteria (Environment, Social, Governance). Companies must provide detailed information on a series of specific indicators for each ESG area. Here is an overview of the main indicators required:

Environmental :

- Greenhouse gas emissions: Companies must report their direct emissions (scope 1), energy-related indirect emissions (scope 2), and other indirect emissions (scope 3).

- Resource use: Includes consumption of water, energy and raw materials.

- Waste management: Quantity of waste produced, management and recycling methods.

- Biodiversity impacts: Effects of the company's activities on local ecosystems and species.

Social :

- Working conditions: Occupational health and safety, accident rates, training and skills development.

- Equality and diversity: Data on employee diversity, non-discrimination policies, equal pay.

- Community involvement: Engagement initiatives with local communities, volunteer programs.

Governance :

- Governance structure: Composition of the Board of Directors, independence of members, diversity on the Board.

- Ethics and compliance: Anti-corruption policies, regulatory compliance measures.

- Financial transparency: Financial disclosure practices, executive compensation policies.

Reporting period and timetable

The CSRD sets precise reporting periods and timetables for the publication of ESG reports. Here are the main stages and deadlines to be respected:

- Large companies: From January 1, 2024, large companies must start collecting the necessary ESG data and publish their first report in accordance with CSRD standards in 2025.

- Listed SMEs: These companies benefit from a transition period and will have to comply with reporting obligations from 2026.

- Subsidiaries of non-European companies: Subsidiaries and branches of non-European companies operating in Europe must comply with CSRD requirements from 2028.

Reporting periods :

- Annual reports: Companies must include ESG information in their annual reports, providing detailed data for the previous year.

- Quarterly updates: Some companies may be required to provide quarterly updates on specific indicators, including those related to critical environmental and social risks.

Verification requirements :

External audit: ESG reports must be verified by an independent third party to ensure the accuracy and reliability of the information provided. This requirement reinforces the credibility of the data reported and ensures compliance with established standards.

Limited assurance: Initially, limited assurance of ESG reports is required, with a possible move towards reasonable assurance as verification capabilities develop.

Adherence to these reporting periods and timetables is crucial for companies, as it ensures not only compliance with regulatory requirements, but also greater transparency and better management of ESG risks.

Benefits and impacts of CSRD

Transparency and stakeholder confidence

One of the key benefits of CSRD is improved transparency and stakeholder confidence. By providing detailed, standardized information on environmental, social and governance (ESG) performance, CSRD enables companies to demonstrate their commitment to sustainability and social responsibility. Here are some key points:

Increased transparency :

- Standardized reporting: Companies must follow clear, uniform reporting standards, making it easier to compare data across companies and sectors. This reduces the risk of greenwashing and increases the credibility of published ESG information.

- Detailed data: Companies are required to provide complete and accurate information on their ESG impacts, enabling investors, regulators and the public to better understand and assess their sustainability performance.

Stakeholder confidence:

- Investors: Investors can make more informed decisions based on reliable ESG data, boosting confidence in companies and their sustainable practices. According to an EY study, 98% of institutional investors evaluate companies' ESG performance before investing.

- Customers and consumers: Consumers are increasingly attentive to companies' sustainable practices. By communicating transparently about their ESG initiatives, companies can strengthen customer loyalty and attract new consumers concerned about the environment and society.

- Employees: Employees, particularly the younger generation, prefer companies whose values are aligned with their own. Greater CSR transparency can improve the commitment and retention of talent within the company.

Impact on corporate strategy

La mise en œuvre de la CSRD a également des impacts significatifs sur la stratégie d'entreprise, obligeant les entreprises à intégrer les considérations ESG dans leur planification stratégique et leurs opérations quotidiennes. Voici comment cela peut influencer la stratégie d'entreprise :

Integrating ESG criteria :

- Strategic planning: Companies must now integrate ESG criteria into their strategic planning. This means identifying and assessing sustainability risks and opportunities, and adapting strategies to maximize positive impacts while minimizing negative ones.

- Objectives and targets: Companies need to set clear sustainability objectives and targets, aligned with ESG standards. These may include reducing greenhouse gas emissions, improving working conditions, or promoting diversity and inclusion.

Innovation and competitiveness:

- Developing sustainable products and services: A focus on sustainability encourages companies to innovate and develop products and services that are more respectful of the environment and society. This can include adopting clean technologies, creating responsible supply chains, and optimizing production processes to reduce waste and emissions.

- Competitive advantage: Companies that adopt sustainable practices can differentiate themselves from competitors and attract ESG-conscious consumers and investors. According to a Deloitte study, companies that integrate sustainability into their strategy enjoy better financial performance and greater resilience in the face of crises.

Risk management :

- Anticipating regulations: By complying with CSRD requirements, companies can anticipate and prepare for future sustainability regulations. This reduces the risk of non-compliance and the costs associated with sanctions and litigation.

- ESG risk reduction: Taking ESG criteria into account enables companies to identify and manage environmental, social and governance risks more effectively. This can include managing climate change risks, protecting human rights, and preventing corruption.

Preparing for CSRD compliance

Key steps in preparation

Preparing for CSRD compliance requires a structured and proactive approach. Here are the key steps to follow to ensure a smooth transition and effective compliance:

Initial assessment :

- Gap analysis: Conduct an assessment of current ESG reporting practices against CSRD requirements. Identify gaps and areas for improvement.

- Data inventory: Collect and centralize all ESG data available within the company. Ensure the quality and reliability of existing data.

Strategy development:

- Develop an action plan: Put in place a detailed plan to address the gaps identified in the gap analysis. Define clear objectives, responsibilities and deadlines for each action.

- Integrate ESG criteria: Integrate ESG criteria into the company's overall strategy. This includes defining policies and procedures for collecting and reporting ESG data.

Internal capacity building :

- Training and awareness: Train employees in CSRD requirements and ESG reporting best practices. Make teams aware of sustainability issues and their role in compliance.

- Creation of a dedicated team: Set up a team responsible for implementing and monitoring ESG initiatives. This team can include members of the HR, finance, legal and operations departments.

Setting up reporting systems:

- Tools and technologies : Adopt ESG data management tools to facilitate the collection, analysis and reporting of information. Digital technologies can help automate and streamline the reporting process.

- Reporting standards: Ensure that ESG reports comply with the standards and guidelines established by the European Sustainability Reporting Standards (ESRS).

Verification and assurance :

- Internal audit: Carry out regular internal audits to verify ESG reporting compliance. Identify potential problems and make the necessary corrections.

- External assurance: Collaborate with external auditors to guarantee the accuracy and credibility of ESG information. This strengthens the confidence of investors and other stakeholders.

Tips for successful implementation

Here are a few practical tips for successful CSRD compliance:

Start early:

- Anticipation: Don't wait until the last minute to start preparing. The earlier a company starts, the more time it will have to adapt to the new requirements and integrate ESG criteria into its operations.

Involve stakeholders:

- Stakeholder engagement: Involve internal and external stakeholders right from the start of the process. Employees, customers, suppliers and investors can provide valuable insights and help identify sustainability priorities.

Adopt an integrated approach:

- Strategic alignment: Integrate ESG criteria into the company's overall strategy. Ensure that sustainability objectives are aligned with business objectives and that all divisions of the company are involved.

Use benchmarks and best practices:

- Sector benchmarking: Compare the company's ESG performance with that of competitors and industry leaders. Use benchmarks to identify areas for improvement and adopt best practices.

Communicate effectively:

- Transparency and clarity: Communicate transparently about sustainability efforts and achievements. Use clear and accessible reports to inform stakeholders of progress made and challenges encountered.

Focustribes supports you in your CSRD compliance projects

Whether you're a company looking to comply with the new requirements of the CSRD directive, or a specialist sustainability consultant, Focustribes is here to help. We support companies in preparing and implementing detailed extra-financial reports in line with European standards. In addition, we help sustainability consultants find assignments that match their skills.

Whether you need to recruit CSRD compliance experts or find freelance opportunities, Focustribes is here to support you throughout your sustainability reporting project.