The European Corporate Sustainability Reporting Directive (CSRD) is based on a central concept: double materiality. This essential concept obliges companies to assess and disclose not only the impacts of their activities on the environment and society, but also how these ESG (environmental, social and governance) issues influence their financial performance. The aim of this directive is to create a more transparent and comprehensive reporting framework, enabling stakeholders to better understand the risks and opportunities associated with sustainability.

Materiality : origin and definition

Origin of materiality

The concept of materiality has its origins in finance, where it is used to identify information that is crucial to investors and other stakeholders. In finance, materiality focuses on data that influence economic decisions, such as financial performance, risks and opportunities. The concept has gradually been adopted by the world of Corporate Social Responsibility (CSR), where it is applied to assess the significance of the environmental and social impacts of a company's activities.

Definition of double materiality

Dual materiality is an extension of the traditional concept of financial materiality, integrating two essential dimensions:

Impact materiality : This dimension assesses the impact of the company's activities on the environment and society. It encompasses aspects such as greenhouse gas emissions, use of natural resources, biodiversity, working conditions and human rights.

Financial materiality : This dimension analyzes how environmental and social issues influence a company's financial performance. This includes risks and opportunities related to ESG issues that may affect the company's stability and profitability.

By integrating these two dimensions, double materiality forces companies to take a holistic view of their impacts and vulnerabilities. This approach, supported by the European Union, has become a core element of CSRD. It is also an integral part of the European Sustainability Reporting Standards (ESRS), reinforcing the importance of this analysis as part of extra-financial reporting.

International and European visions

ISSB: an international vision

The International Sustainability Standards Board (ISSB) proposes an investor-focused approach to materiality. This international vision focuses on how ESG issues affect a company's financial performance. The ISSB seeks to standardize sustainability reporting to ensure that investors have the information they need to assess the financial risks and opportunities associated with ESG factors. This perspective focuses on financial materiality and how ESG elements influence investors' economic decisions.

EFRAG: the European vision

The European Financial Reporting Advisory Group (EFRAG) has adopted a more integrated approach, based on dual materiality. This European vision includes not only financial materiality, but also impact materiality. This means that companies must assess and report not only how ESG issues affect their financial performance, but also how their activities impact the environment and society. This approach is supported by the CSRD and ESRS standards, aimed at providing greater transparency and greater consideration of sustainable issues by all stakeholders.

EFRAG's dual materiality approach makes it possible to understand not only the financial risks and opportunities associated with ESG issues, but also the broader implications of these issues on the company's entire ecosystem. This vision is in line with the European Union's sustainability objectives, which seek to promote a more sustainable and resilient economy.

Why do a double materiality analysis ?

Regulatory obligations

The main reason for carrying out a dual materiality analysis is to comply with the regulatory requirements imposed by the CSRD. The directive requires eligible companies to assess and disclose both the impact of their activities on the environment and society (impact materiality) and the impact of ESG issues on their financial performance (financial materiality). This means that companies must integrate this analysis into their extra-financial reports to meet European ESRS standards.

Strategic advantages

Beyond regulatory compliance, double materiality analysis offers several strategic advantages for companies:

- Anticipating risks and opportunities: By assessing environmental, social and financial impacts, companies can better anticipate ESG-related risks and identify opportunities for sustainable growth. This enables better risk management and more informed decision-making.

- Improved resilience: Integrating ESG issues into corporate strategy helps to build resilience to environmental and social crises. A well-prepared company is better able to adapt to change and maintain its performance over the long term.

- Enhanced transparency and stakeholder confidence: Detailed and transparent reporting on ESG impacts and their influence on financial performance improves the confidence of investors, customers and other stakeholders. It can also enhance a company's reputation and attract responsible investment.

Which companies will be subject to the double materiality analysis ?

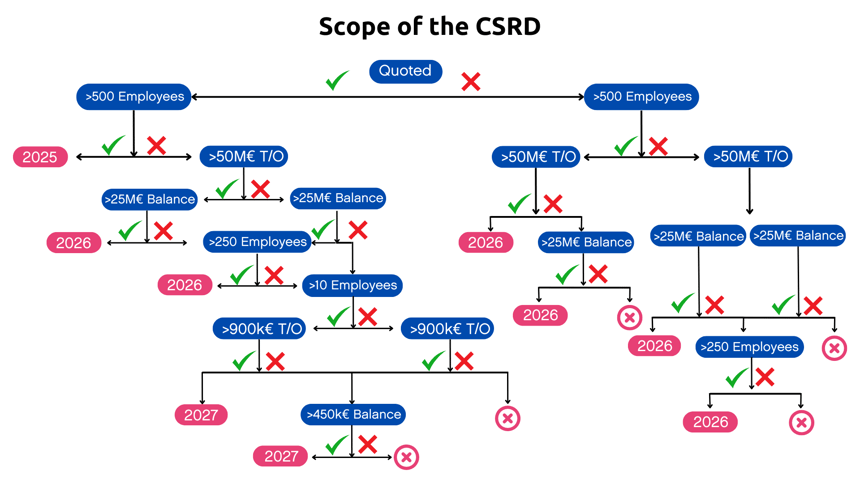

The scope of the CSRD extends to a much larger number of companies than the previous directive, the NFRD. The categories of companies concerned include large corporations, listed SMEs and certain non-European companies with significant activity in Europe. The chart below shows the specific criteria and implementation dates for each category of company.

How do you prepare to a double materiality analysis ?

Step 1: Identify the issues to be analyzed

The first step in preparing a double materiality analysis is to identify the environmental, social and governance (ESG) issues relevant to the company. This involves listing all the potential impacts of the company's activities and prioritizing them according to their importance and relevance for stakeholders and for the company itself.

It is crucial to draw up an exhaustive list of possible issues, and to rank them according to their severity and probability of occurrence.

Step 2: Consult with stakeholders

Stakeholder consultation is an essential step in obtaining a comprehensive and relevant view of ESG issues. This consultation provides information on the expectations and concerns of stakeholders such as employees, customers, suppliers, investors and local communities.

Involving stakeholders in the consultation process helps to identify the most significant issues and to understand different perspectives.

Step 3: Using EFRAG's methodology to assess the materiality of an issue

EFRAG provides clear guidelines for assessing the materiality of ESG issues. Using this methodology ensures a rigorous and consistent assessment of impacts, based on standardized and recognized criteria.

Using the standards and criteria defined by EFRAG therefore ensures a structured analysis that complies with regulatory requirements.

Step 4: Formatting the dual materiality analysis

The final step is to summarize the results of the dual materiality analysis in a clear, structured report. It is important to present the information in a transparent and accessible way, highlighting the main issues identified and their impact on the company and its stakeholders.

The report should be written in such a way as to be comprehensible to all stakeholders, highlighting the main conclusions and recommended actions.

Focustribes can help you prepare your double materiality analysis

Whether you're a company looking to comply with the new requirements of the CSRD or a specialist sustainability consultant, Focustribes is here to help. We support companies in preparing and implementing detailed extra-financial reports in line with European ESRS standards. We also help sustainability consultants find assignments that match their skills.

Do you need to recruit CSRD compliance experts or find freelance opportunities? Focustribes is here to support you throughout your sustainable reporting project.