The transition from the Extra-Financial Performance Declaration (EFPR) framework to the Corporate Sustainability Reporting Directive (CSRD) represents a major turning point in the field of extra-financial reporting for companies. Although these two directives have similar objectives, they differ in several respects, particularly in terms of requirements and the companies concerned. Understanding these differences is essential for companies to prepare adequately and take advantage of the opportunities offered by these new regulations.

Non-financial reporting context

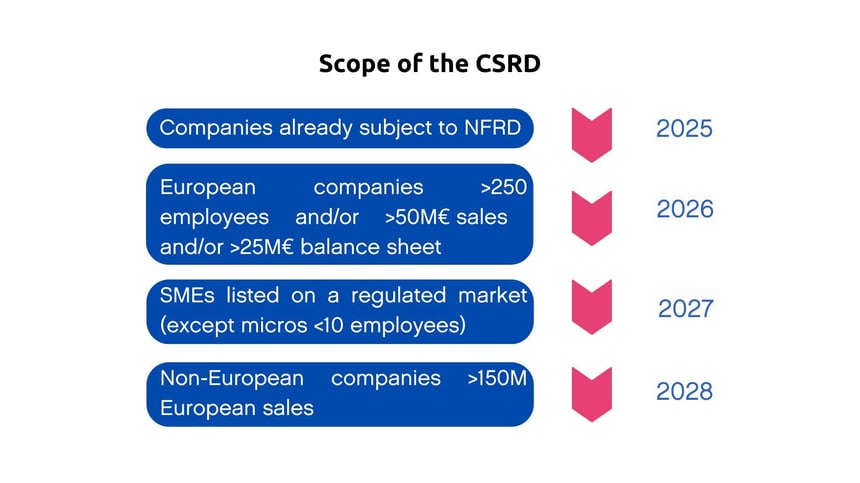

Evolution from NFRD to CSRD

The Non-Financial Reporting Directive (NFRD), adopted in 2014, was the first European directive to impose extra-financial reporting obligations on large companies and public interest entities. However, as environmental and social issues have evolved, the NFRD has shown its limitations in terms of the scope and accuracy of the information provided. In response, the CSRD was introduced to replace and reinforce the NFRD. Adopted in 2021, the CSRD extends reporting requirements to a wider range of companies, including large unlisted companies and listed SMEs, and introduces more stringent and detailed reporting standards.

DPEF in France

In France, the EPFD was set up to transpose the requirements of the NFRD. Since 2017, it has required companies with more than 500 employees and a turnover of more than €100 million to publish information on their environmental, social and governance (ESG) performance. The EPFD focuses on areas such as environmental impacts, social and societal issues, respect for human rights and the fight against corruption. With the introduction of the CSRD, the DPEF is set to evolve to incorporate the new requirements of the European directive.

The objectives of the CSRD and the DPEF

Objectives of the DPEF

The main aims of the EPFD are :

Transparency: Increase the transparency of companies' ESG performance.

Risk Management: Enabling companies to identify and manage ESG risks.

Improved Performance: Encourage companies to improve their ESG performance

Stakeholder Confidence: Strengthen the confidence of investors, customers and other stakeholders through detailed and transparent reporting.

Objectives of the CSRD

The CSRD has more ambitious and far-reaching objectives:

Harmonisation of Standards: Establish uniform and comparable reporting standards across the European Union.

Broadening the Scope: Include around 50,000 companies in Europe, compared with 11,000 for the NFRD.

Dual Materiality: Consider both the impact of companies' activities on the environment and society, as well as the impact of ESG issues on their financial performance.

Certification of Reports: Requiring the certification of sustainability reports by an independent third party to guarantee the reliability of the information published.

Reporting obligations and ESG standards

ESG indicators required

The CSRD imposes specific ESG indicators that companies must include in their reports. These indicators cover various aspects such as carbon emissions, water management, diversity and inclusion, and ethical governance.

Reporting period and calendar

Companies must comply with specific reporting periods, with annual reports detailing their ESG performance. The reporting calendar is aligned with companies' financial years to ensure consistency in the presentation of data.

Benefits and challenges of compliance

Transparency and trust

The CSRD aims to improve the transparency of companies, thereby strengthening the confidence of investors, consumers and other stakeholders. Greater transparency makes it easier to assess the risks and opportunities associated with sustainability.

Impact on corporate strategy

CSRD encourages companies to integrate ESG criteria into their overall strategy, thereby improving their resilience and competitiveness. Companies need to adapt their practices to meet the new requirements, which can lead to innovation and operational improvements.

Preparing for CSRD compliance

Key steps to prepare

Initial Assessment: Companies should begin by assessing their current compliance with CSRD requirements and identifying gaps that need to be addressed.

Policy Development: Develop internal policies and procedures to align company practices with CSRD requirements.

Training and Awareness: Train and raise employee awareness of new reporting requirements and ESG practices.

Tips for a successful implementation

Stakeholder engagement: Involve internal and external stakeholders to ensure effective implementation and obtain valuable feedback.

Use of technology tools: Use technology tools to facilitate the collection, analysis and reporting of ESG data.

Monitoring and continuous improvement: Implement monitoring and evaluation mechanisms to measure progress and continuously improve reporting practices.

Focustribes can help you with your CSRD compliance projects

Whether you are a company looking to comply with the new requirements of the CSRD or a specialist sustainability consultant, FocusTribes is here to help. We support companies in preparing and implementing detailed extra-financial reports in accordance with European standards. We also help sustainability consultants find assignments that match their skills.

Whether you need to recruit CSRD compliance experts or find freelance opportunities, FocusTribes is here to support you throughout your sustainability reporting project.